Breaking businesses based on life cycle ( Hypergrowth , Growth and Value)

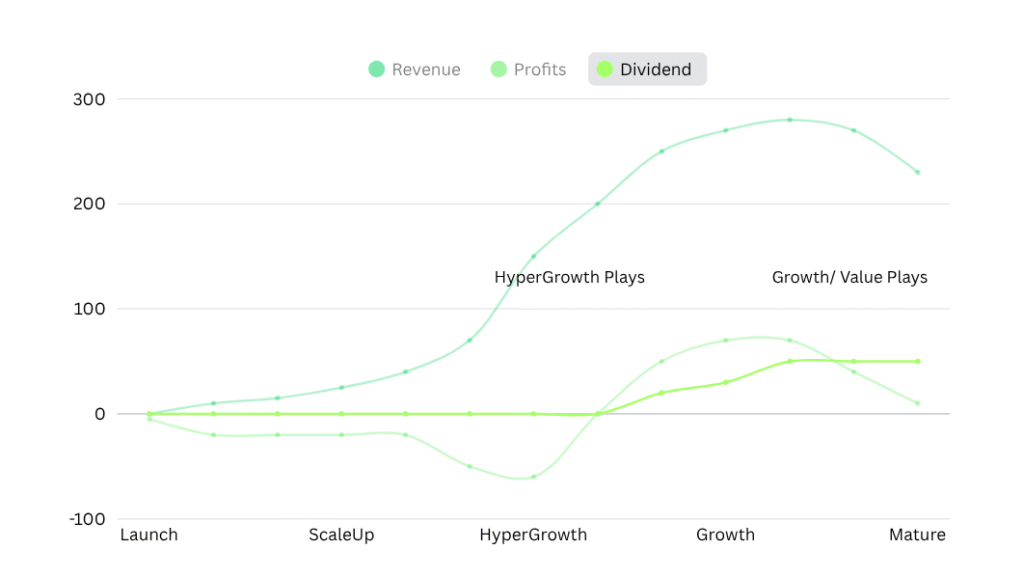

Every company goes through a simple lifecycle. It starts at Launch with high risk and no profits, then moves into ScaleUp where growth accelerates. The Turning Point is when the business finally becomes profitable. The Growth stage is where compounding happens and returns are strongest. Eventually, companies reach Mature/Death, where growth slows and profits decline.

Early in the growth stage, cash is tight and companies rarely pay dividends. Later in the mature stage, dividends usually rise but often at the cost of slowing growth and weakening business fundamentals.

I split my investing into three categories: Value , Growth and HyperGrowth Stocks.

Portfolio Allocation , How This Fits My Singaporean Context Portfolio

As a Singapore-based investor, I prioritise investments that are tax-efficient and suitable for the local regulations I operate under. At the same time, I’m naturally risk-averse, so my allocation leans toward stability, dividends, and long-term compounding rather than aggressive speculation.

My portfolio reflects this balance: strong income-generating Value stocks, steady Growth names, and a small, controlled allocation to HyperGrowth opportunities.

| Category | Business Type | Key Metrics | Regions I Prefer | Examples |

|---|---|---|---|---|

| Value (60–70%) | Mature, stable, low volatility | PE, D/E, cash flow, margins | SG / MY / HK / UK | GSK, Link REIT, Singapore banks |

| Growth (20–30%) | Expanding, improving fundamentals | PEG, margin expansion, FCF | HK / US | PayPal, Bosideng, Alibaba, Google |

| HyperGrowth (5–10%) | Fast-scaling, disruptive, early-stage | NRR, TAM, user growth, runway | Mostly US | Udemy (more to be added) |

Angpow Investor Portfolio based on Peter Lynch Categories: How the Company Behaves

I use Peter Lynch’s framework because it helps me understand how each company behaves whether it’s a steady stalwart, a cyclical mover, a fast grower, or a turnaround story. It keeps my expectations realistic and my investing decisions simple and disciplined.

| Category | Definition | My Stocks Picks |

|---|---|---|

| Stalwarts | Stable, mature, predictable earnings; low–moderate growth | Heineken Bhd, Merck, GSK, Pfizer, Lululemon, Flowers Foods, Carlsberg MY, Utah Medical |

| Cyclicals | Earnings tied to economic cycles; boom–bust patterns | Delfi, Genting SG, Bosideng, Samsonite, Burberry, Mengniu Dairy, Baidu, Kuaishou, Xtep, Sun Hung Kai Props, HongkongLand, China Overseas Property, Paycom |

| Value / Turnaround | Mispriced stocks with temporary issues; improving fundamentals | PayPal, Global Payments, Fiserv, T. Rowe Price, Alibaba, Edvantage, Fu Shou Yuan, SSY Group, Ashmore, CK Hutchison, Upwork |

| Fast Growers | 20–50% revenue/earnings growth; scaling companies | Alphabet, Lululemon, NetEase, Upwork, Xtep, Haier Smart Home |

| Hyper-Growth | Loss-making or high-PE moonshots with big upside | Udemy, (partially: Baidu AI, Kuaishou) |

| Slow Growers / Defensive | Low growth but steady cash flow; dividend-oriented | ThaiBev, PSC Corporation, Oi Wah Pawnshop, Water Oasis, China BlueChemical |

| Asset / NAV Plays | Value driven by property, NAV discount or hard assets | HongkongLand, Sun Hung Kai Properties, CK Hutchison, Miramar Hotel, King Fook, Link REIT, Yuexiu Services |

How My Portfolio Performed in 2025 (Summary)

2025 was a surprisingly strong year for my portfolio, driven mainly by a broad recovery in Hong Kong equities and steady performance from my stalwart and dividend positions.

⭐ 1. Hong Kong Outperformed Strongly

✅ THE GOOD — Strong Performers & Outperformers

1. Hong Kong Deep Value & Asset Plays Led the Portfolio

This was the strongest theme of the year.

| Stock | Gain | Why It Worked |

|---|---|---|

| Hong Kong Exchange (HKEX) | +70.1% (+76.5% incl. dividends) | Benefited from HK market recovery, liquidity improvements |

| HongkongLand | +93.1% (+101.7% incl. dividends) | Massive NAV discount narrowing; property sentiment improving |

| CK Hutchison | +37.8% (+43.1%) | Conglomerate rerating; strong yield |

| Sun Hung Kai Properties | +26.9% (+31.7%) | Rebound in HK real estate |

| King Fook | +42.3% (+50.6%) | Jewelry + property play benefiting from tourism rebound |

| Miramar Hotel | +8.4% (+15.1%) | Hotel/tourism recovery improving occupancy and margins |

| Johnson Electric (Sold) | +212.0% (+5%) | One of the highest individual performers; benefited from industrial cycle rebound, strong operating leverage, and valuation uplift from deep cyclical lows. |

Theme:

Deep value, property-linked, and NAV-discount stocks in Hong Kong delivered exceptional returns, validating the Value + Asset Play thesis.

2. U.S. Growth and Fast-Growers Returned to Form

Finally, U.S. growth stopped derating and started compounding again.

| Stock | Gain | Why It Worked |

|---|---|---|

| Alphabet | +105.5% | Strong AI leadership, excellent earnings, valuation uplift |

| Upwork | +57.1% | Cost discipline + demand recovery |

| NetEase | +66.5% (+70.7%) | Strong gaming pipeline, steady margins |

| Lululemon | +13.1% | Strong global demand and brand expansion |

Theme:

Quality Growth is working again, especially names with strong cash flow and durable moats.

3. Cyclical Retail & Consumer Plays Performed Well

Strong rebounds in China & Southeast Asia consumer spending:

| Stock | Gain |

|---|---|

| Best Mart 360 | +26.9% (+40.0%) |

| Bosideng | +29.9% (+35.6%) |

| Samsonite | +38.3% (+44.3%) |

| Leong Hup | +21.1% |

Theme:

Cyclicals worked because the timing was right , economy reopening, tourism picking up, and consumer spending recovering.

❌ THE BAD — Underperformers & Still awaiting turnaround

Not every part of the portfolio delivered in 2025. Some sectors were hit by structural issues, some are in long-term turnaround mode, and others are simply tied to a slowing consumer cycle. These weaknesses are important to acknowledge, because they reveal where risk remains and where patience is required.

1. China Education, Property Services & Funeral Sector Dragged Returns

These sectors continue to face regulatory and demand pressure.

| Stock | Loss | Reason |

|---|---|---|

| Edvantage | -26.4% | For 2025, Edvantage reported a drop in gross profit and a significant increase in costs (teacher salaries, facility upgrades, expansion) |

| Yuexiu Services | -12.0% | Property mgmt margins shrinking |

| SSY Group | -13.4% | Generic pharma price pressure |

| Anxian Yuan | -13.7% | Low-volume illiquid stock; China funeral industry slowdown |

Lesson:

Although majority of china has rebounded quite nicely . The funeral sector, property remain laggards….

2. U.S. Payment Turnarounds Still Not Turning

These companies remain fundamentally strong, but the market simply doesn’t love payment processors right now. With U.S. consumer discretionary spending slowing, the entire payment industry has taken a hit.

| Stock | Loss |

|---|---|

| PayPal | -8.1% |

| Global Payments | -7.4% |

| Fiserv | -1.9% |

Lesson:

Turnarounds take time.

The earnings recovery hasn’t shown up yet, and the sector sentiment remains soft.

3. U.S. Healthcare Defensives Are Massively Undervalued

Healthcare in the U.S. is currently one of the most discounted sectors. Strong businesses, but out of favour.

| Stock | Loss |

|---|---|

| Pfizer | -12.2% |

| Utah Medical | -18.6% |

Lesson:

The sector is attractively valued , not broken, just unloved. This may offer long-term opportunity rather than risk.

4. U.S. & Global Cyclicals Feeling the Slowdown

Consumer-linked businesses across the board are showing signs of stress. Even companies with good fundamentals are struggling due to weakening global demand.

| Stock | Loss |

|---|---|

| Genting Singapore | -7.0% |

| Man Wah | -7.1% |

| Flowers Foods | -14.9% |

| Domino’s UK | -11.8% |

Lesson:

Cyclicals require good timing, and right now the consumer cycle is clearly slowing. This affects travel, furniture, packaged foods, and discretionary spending , a broad weakening across the cycle.

🔭 What I’m Watching Going Forward

2025 has been a year of learning and recalibration. The strong rebound in Hong Kong and the steady performance of my value holdings showed me the value of dividend investing and consistency … the value of just Keep Buying!

But the biggest shift this year is my growing interest in U.S. opportunities again.

⭐ 1. U.S. Stocks Are Becoming Attractive Again

Valuations in several high-quality U.S. names have reached levels I haven’t seen in years. These companies have strong fundamentals, durable moats, and long-term compounding potential.

On my watchlist:

- NVO (Novo Nordisk) – Weight-loss megatrend + pricing power

- PayPal – Still a cash machine; valuation compressed

- Shift4 Payments – Hyper-growth merchant acquiring

- Global Payments (GPN) – Undervalued, steady enterprise payments

- Fiserv – Quiet compounder in the fintech/payments ecosystem

Reflection:

The U.S. is offering a rare mix of quality + reasonable valuations — something I haven’t seen since 2015–2016.

⭐ 2. Exploring HyperGrowth , Slowly and Carefully

I’ve begun studying hypergrowth companies more seriously, especially SaaS names where:

- Okta , Grab , Duolingo

But I’m still very early in this journey. Not really sure how to evaluate it , seems like EV/Sales and ProfitMargin . Or adhering to the Rule of 40 might be a good approach. The possible price swing scares me, so im really not sure if i will pull the trigger but let see…