My dad is 61 this year and recently he was thinking about buying a 1.1mil investment condo unit in Singapore. In this blog post, i will attempt to run the numbers to see if this might be a viable financial decision.

Step1: Can He Buy It?

Step1.1 Loan Eligibility

Figuring out loan eligibility can be confusing, and one way is to start with a home loan calculator.

- Uob Home loan Calculator – https://forms.uob.com.sg/property/calculator/

- Dbs Home loan Calculator – https://www.dbs.com.sg/personal/marketplace/property/plan/selection

|  |

As my dad is a bit older, I reached out to several loan specialists to get an IPA (In-Principle Approval):

- UOB mortgage agent

- DBS home loan agent

- Redbrick Mortgage Advisory consultant

There were also some useful insights shared during my discussions with the loan agents. If your declared income is not sufficient, some banks may consider your cash holdings and overall financial position to strengthen the application.

As a older buyer , he faced a shorter loan tenure.

Because of his age, the likely financing outcome for a 1.1mil invesment condo is:

- Max Loan: 55%

- Loan Amount: S$605k

- Downpayment: S$495k

- Tenure: ~14 years

This means he will have to fork out a higher monthly installment of roughly how much based on interest rate

Step 1.2 Estimated Monthly Mortgage (S$605k over 14 years)

I used the repayment calculator from DBS to estimate the monthly mortgage for a S$605,000 loan over 14 years.

Mortgage Stress Test Scenarios

Interest rates fluctuate over time, so it is important to run different scenarios before committing to a property purchase.

For my dad’s S$605,000 loan over 14 years, I used the following interest rate assumptions to test affordability:

| Interest Rate | Scenario | Estimated Monthly Mortgage Rate |

|---|---|---|

| 1.5% | Best case / current low rate | ~ $3,995 |

| 2.5% | Favourable normal case | ~ $4,272 |

| 3.5% | Neutral long-term case | ~ $4,560 |

| 4.5% | Stress test case | ~ $4,860 |

| 5.0% | Severe downside case | ~$5,015 |

The key takeaway is that even small interest rate changes can materially impact monthly cash flow, so financing cost is a major factor in determining whether the investment makes sense.

Step 1.3: How Much Cash Needed Upfront?

With the loan eligibility in mind, I then started budgeting for the upfront cash required, assuming zero CPF usage.The next question was simple:

How much cash would my dad need on hand to comfortably proceed with the purchase?

For a 1.1million condo:

| Item | Estimated Amount |

|---|---|

| Downpayment (45%) | S$495,000 |

| Buyer’s Stamp Duty (BSD) Useful Tools: Buyer Stamp Duty Calculator | ~S$28,600 |

| Legal Fees | ~S$3,000 – S$5,000 |

| Valuation / Admin Fees | ~S$1,000+ |

| Buyer Agent Commission (1%–2%) | S$11,000 – S$22,000 |

| Basic Furnishing / Touch-up Buffer | S$5,000 – S$15,000 |

This comes up to around S$543,000 to S$567,000+

Step 1.4 important note: Source of Funds & Compliance Checks

As with any property purchase, buyers should also expect standard anti-money laundering (AML) and compliance checks.

This means you may need to demonstrate the source of funds / source of wealth used for the purchase.

Typical examples include:

- Salary savings

- Business income

- Investment proceeds

- Sale of previous property

- Inheritance or gifts (with supporting records)

It is helpful to maintain:

- Clear bank statements

- Traceable transaction history

- Supporting documents for large transfers

Conclusion of Step1 : Can he buy it?

Yes, he likely can buy it, if he has the available cash, passes financing checks, and is comfortable with the repayment burden.

Step 2: Can He Afford the Monthly Mortgage?

(After Considering Rent & Vacancy)

Buying the condo is one thing. Holding it comfortably every month is another.

The key question becomes: Can he afford the monthly mortgage even if rental income is inconsistent?

Step 2.1 Gross Rental Yield

Gross rental yield measures rental income before expenses.

Gross Yield = Annual Rent ÷ Purchase Price

For a S$1.1M condo, the rental yield looks like this:

| Monthly Rent | Annual Rent | Gross Rental Yield |

|---|---|---|

| S$3,500 | S$42,000 | 3.82% |

| S$4,000 | S$48,000 | 4.36% |

| S$4,500 | S$54,000 | 4.91% |

| S$5,000 | S$60,000 | 5.45% |

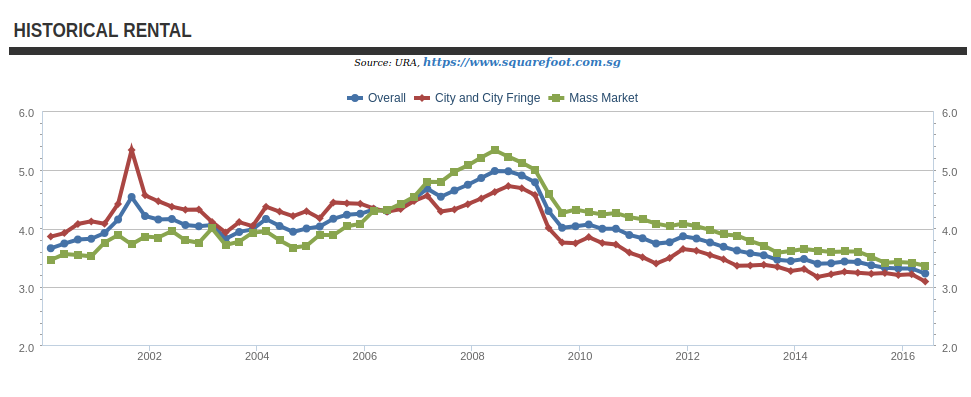

based on singapore market history

Step 2.2 Estimated Monthly Holding Cost (Excluding Mortgage)

Rental income is not pure profit. There are recurring ownership costs even before loan repayments.

I estimate monthly holding costs at around: ( this varies project to project)

| Item | Estimated Monthly Cost |

|---|---|

| Condo Maintenance (MCST) | S$380 |

| Property Tax (Investment Use) | S$230 |

| Insurance | S$25 |

| Repairs / Maintenance Reserve | S$120 |

| Vacancy / Leasing Reserve | S$300 |

| Total Monthly Holding Cost | S$1,055 |

Step 2.3 Net Rental Yield

Net rental yield accounts for recurring property costs.

Net Rent = Gross Rent – Annual Holding Costs

Annual holding cost:

| Monthly Rent | Annual Rent | Gross Rental Yield | Net Annual Rent | Net Rental Yield |

|---|---|---|---|---|

| S$3,500 | S$42,000 | 3.82% | S$29,340 | 2.67% |

| S$4,000 | S$48,000 | 4.36% | S$35,340 | 3.21% |

| S$4,500 | S$54,000 | 4.91% | S$41,340 | 3.76% |

| S$5,000 | S$60,000 | 5.45% | S$47,340 | 4.30% |

Net Rental Yield Thoughts

I was an avid reader of No B.S. Guide to Property Investing, where the author often mentioned targeting a 5% net rental yield.

Honestly, in today’s Singapore market, that sounds quite difficult to achieve for many private condos.

With higher property prices, rising ownership costs, and compressed yields, hitting a true 5% net yield now is far less common than in previous years.

This may simply reflect a different property cycle.

There were periods in the past where lower entry prices and stronger rents made 5% net yields more realistic

Looking Back at Singapore Market History

| Period | Market Conditions | Typical Yield Environment |

|---|---|---|

| 2009–2012 | Post-GFC lower prices, rents recovered quickly | Strong yields, 5% net more possible selectively |

| 2013–2017 | Cooling measures softened prices | 4%+ gross easier, selective high net yields |

| 2018–2021 | Prices climbed, rents softer | Yield compression |

| 2022–2023 | Rental surge across Singapore | Existing owners enjoyed sharp yield jump |

| 2024–2026 | Prices high, rents stabilising | Gross 3%–5%, net harder to stretch |

Step 2.4

Forecasted Capital Appreciation (And Yes — Prices Could Also Fall)

Rental yield gives cashflow, but capital appreciation is what often creates the bigger wealth outcome over time.

No one can know for certain, but based on current market forecasts, most analysts expect moderate growth rather than explosive gains.

Recent market commentary suggests private residential prices may rise around 2%–4% in 2026, after a slower 3.3% growth in 2025.

| Annual Growth Rate | 5-Year Estimated Value | Gain |

|---|---|---|

| 2% / year | S$1.214M | +S$114k |

| 3% / year | S$1.275M | +S$175k |

| 4% / year | S$1.338M | +S$238k |

| 5% / year | S$1.404M | +S$304k |

Its anyone guess , prices might fall instead!

In a bear case

| Annual Growth Rate | 5-Year Estimated Value | Gain / Loss |

|---|---|---|

| -3% / year | S$945k | -S$155k |

| -2% / year | S$994k | -S$106k |

| -1% / year | S$1.046M | -S$54k |

| 0% / year | S$1.100M | S$0 |

| 2% / year | S$1.214M | +S$114k |

| 3% / year | S$1.275M | +S$175k |

So, picking the right property is extremely important in the decision-making process.

A successful investment is not just about buying any condo — it is about choosing the right asset while considering the wider market environment.

Key factors to watch include:

- Interest rate direction – affects mortgage affordability and buyer demand

- Inflation trends – influences rents, costs, and monetary policy

- Holding power – ability to comfortably hold through vacancies or slower markets

- Entry price – buying well matters

- Rental demand – determines income consistency

- Location quality – supports both rentability and resale value

In many cases, the investor who buys the better unit outperforms the investor who simply buys during the “right market.” A huge part of the risk lies here, if u pick the right project , at the right macro time , ur investment will do well if not u might get a laggard and potentially even a loser!

I will expand on this section as this might be tough to predict

Step3 The opportunity cost.

If S$540k Invested in S&P 500 for 5 Years

| Annual Return | 5-Year Value | Gain |

|---|---|---|

| 4% | S$657k | +S$117k |

| 6% | S$723k | +S$183k |

| 8% | S$793k | +S$253k |

| 10% | S$870k | +S$330k |

If condo bought at S$1.1M for 5 years

- Gross Rental yield: 4.36%

- Net rental yield: 3.21% (based on S$4,000 rent model)

- Net annual rent: S$35,340

| Scenario | Annual Price Growth | 5-Year Property Value | Capital Gain / Loss | 5-Year Net Rental Income | Total Economic Gain |

|---|---|---|---|---|---|

| Bear Case | -1% | S$1.046M | -S$54k | S$176.7k | S$122.7k |

| Flat Case | 0% | S$1.100M | S$0 | S$176.7k | S$176.7k |

| Base Case | 2% | S$1.214M | +S$114k | S$176.7k | S$290.7k |

| Good Case | 3% | S$1.275M | +S$175k | S$176.7k | S$351.7k |

| Bull Case | 4% | S$1.338M | +S$238k | S$176.7k | S$414.7k |

Final Thoughts

Buying a property entails far more effort than simply lump-sum investing into the S&P 500.

With property, there are transaction costs, financing risk, tenant management, maintenance issues, and lower liquidity when exiting.

Because of this, it would only make financial sense if we arereasonably confident the investment can achieve at least a Good Case outcome