Barely a week after I deployed capital into a basket of hypergrowth SaaS and fintech stocks, the market reminded me of one brutal truth:

Timing the short term is impossible.

My portfolio packed with names like GitLab, Trade Desk, HubSpot, Adobe, Shift4, and Remitly suddenly turned red. Losses appeared almost immediately:

- PayPal: -40%

- Paycom: -20%

- GitLab: -16%

- Trade Desk: -15%

- Global Payments: -16%

- HubSpot: -14%

- Udemy: -13%

- Adobe: -11%

- Shift4: -7%

- Remitly: -6%

It definitely doesn’t feel good watching fresh positions drop so quickly.

Thankfully, my overall portfolio is still solidly green, a strong reminder of why position sizing and diversification matter. When growth stocks correct, the rest of the portfolio acts as a stabilizer.

This episode reinforces a simple investing truth:

The game isn’t about avoiding drawdowns entirely.

It’s about managing them while still capturing long-term upside.Reducing price drawdown while ensuring good returns ,

that’s the real trick of the game.

From China Tech Crash to SaaS Armageddon , Why Position Sizing Became My Investing Rule #1

Markets have a way of humbling investors not once, but repeatedly.

I’ve lived through multiple “mini-armageddons” in my portfolio in recent years:

- The China tech crackdown, when Alibaba and peers collapsed far faster than fundamentals seemed to justify (from about $300 to $61.05)

- The banking panic in 2021, when financials suddenly looked fragile overnight (Citibank plunging from around $70 to crisis lows)

- The luxury meltdown, when names like Burberry saw sharp valuation resets

- And now, the recent SaaS selloff, hitting hypergrowth software and fintech almost immediately after I entered positions

Each episode felt different at the time.

Different headlines. Different narratives. Different sectors.

But in hindsight, they all taught me the same lesson:

Stock picking matters. But position sizing matters more.

🧨 The Alibaba Lesson I Learned the Hard Way

I was one of the victims of Alibaba.

What started as conviction slowly turned into revenge averaging.

I bought at what felt like great prices:

- $150 looked cheap

- $120 looked even better

- $90 felt like a bargain

But the stock kept sinking.

$80…

$70…

$60…

By the time it bottomed, I had deployed most of my capital trying to “average down”.

I wasn’t just wrong on timing.

I had run out of bullets.

At one point, Alibaba alone was close to 50% of my portfolio.

That was the real mistake.

Not the company.

Not the thesis.

The size.

Because once a single position becomes that large:

- Every price movement feels personal

- Objectivity disappears

- Decision-making becomes emotional

- And your portfolio’s fate becomes tied to one story

That experience permanently changed how I invest.

🧠 The Pattern I Eventually Notice

Every crash followed a similar structure:

- A sector becomes popular

- Valuations expand

- Something changes regulation, rates, sentiment, or macro fear

- The whole sector drops together

Not because every company suddenly became bad.

But because capital rotates fast.

And when a whole sector sells off:

- Owning multiple China tech names doesn’t protect you

- Holding several SaaS companies doesn’t diversify you

- Buying many growth stocks in one theme still equals concentration

The illusion of diversification disappears.

What matters most is:

How big each position — and each sector — really is.

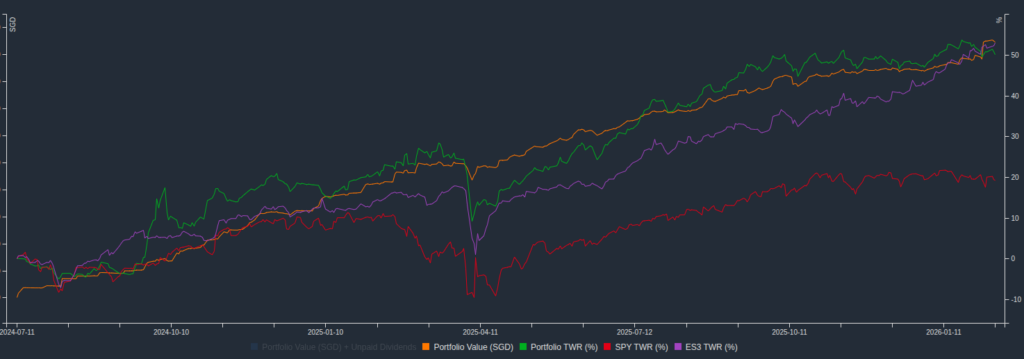

In the chart above, the orange line represents my portfolio.

It’s not perfect, and it certainly hasn’t avoided volatility. But over time, dollar cost averaging, diversification and better position sizing have helped soften the drawdowns and make the portfolio more stable during market swings.

The goal was never to eliminate losses entirely that’s impossible.

Instead, it was to reduce the severity of downturns while still allowing the portfolio to grow.

Looking at the orange line, I’m grateful that the performance of my portfolio remains really stable but also outperforming the indexes. Only time will tell if this will continue and hopefully it will end up on the greener side!

Reflecting on My Position Sizing Strategies

After a recent conversation with some wiser friends in my investing Telegram group, the topic of concentration risk came up. It made me pause and reflect on my own approach and I felt it was a good time to pen down how I think about position sizing going forward.

1️⃣ Capping Sector Exposure

One of the biggest lessons I’ve learned is to stay actively aware of sector exposure, especially in areas like hypergrowth SaaS where price-drawn of up to 70-90% is part of the game.

Each sector gets a soft ceiling in my portfolio.

If exposure is already high, any new buys must be smaller or skipped entirely.

This helps prevent the situation where I unknowingly build a large bet on a single theme, even if it’s spread across multiple stocks.

2️⃣ Always Start Small & Pre-Define the Maximum Size

I rarely open a full position on day one.

Instead, I:

- Start with a starter position

- Watch earnings, sentiment, and execution

- Add only if the thesis strengthens

This keeps optionality alive and prevents emotional overcommitment too early.

3️⃣ Define the Maximum Size Upfront

Before buying, I decide:

- What’s the ideal position size

- What’s the absolute maximum allocation

Once the max is reached:

No more averaging down. No exceptions.

This rule exists because I’ve learned firsthand what happens when limits aren’t set in advance.

Addressing the SaaS Armageddon, Revisiting My Stock Picks Again

As i revisit my stock picks again, i like to reevaluate if this ai fears has become real.

What’s really killing software stocks

Three big fears are driving the sell-off:

🔥 Fear #1: “AI agents make software free”

Tools like Claude agents, Copilot Studio, etc. make people think:

“Why pay Adobe / Salesforce / Atlassian when I can just build it myself?”

This hits UI-heavy tools hardest.

🔥 Fear #2: Seat-based pricing breaks

Classic SaaS:

- 1 employee = 1 license

AI world:

- 1 human + 10 AI agents = fewer licenses

So investors fear:

Revenue ↓ even if customers stay

🔥 Fear #3: Everyone panics at once

Markets don’t discriminate short-term:

- “AI bad → sell all software”

- Baby + bathwater situation

This is exactly what happened with Nvidia (DeepSeek) and Google vs ChatGPT before they ripped higher.

The 3-Layer SaaS Framework

Every serious software company provides one or more of these layers:

| Layer | Meaning | AI Risk |

|---|---|---|

| System of Record (SoR) | Legal, financial, audit-grade data | 🟢 Low |

| System of Engagement (SoE) | UI, dashboards, workflows | 🔴 High |

| System of Intelligence (SoI) | Agents, automation, orchestration | 🟡 Medium |

🟢 Infrastructure & Control Layer (AI Beneficiaries)

These companies power AI itself.

- Amazon → AI runs on AWS.

- Meta → AI improves ad targeting and monetization.

- ServiceNow → AI agents operate inside enterprise workflows.

- Zscaler → AI increases cybersecurity demand.

- Vertiv → AI requires data centers.

🟡 Platform & Ecosystem Layer (AI Enhances Efficiency)

These companies operate platforms, not seat-based SaaS.

- Sea / MercadoLibre → AI improves logistics, ads, fraud detection.

- Grab → AI optimizes routing and pricing.

- Atlassian / GitLab → AI coding increases workflow usage.

- The Trade Desk → AI drives automated ad bidding.

🔴 Engagement & Human Productivity Layer (Highest Risk)

This is where AI pressure is real.

- Adobe → AI-native creative tools reduce designer seats.

- Udemy → AI tutors personalize learning.

- Upwork → AI replaces entry-level freelancers.

- HubSpot → AI compresses marketing headcount.

| Rank | Company | SOR | SOE | SOI | AI Risk | Elaborated Structural Summary |

|---|---|---|---|---|---|---|

| 1 | Amazon | ⭐⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐⭐ | Very Low | Owns AWS infrastructure. AI demand directly increases cloud usage, compute, and inference. Not seat-based. Structural beneficiary. |

| 2 | Meta | ⭐⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐⭐ | Very Low | AI strengthens ad targeting, monetization, and content ranking. Owns AI stack + data graph. Not productivity dependent. |

| 3 | ServiceNow | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐⭐ | Very Low | Deep enterprise workflow SOR. AI agents operate inside platform. Extremely sticky due to compliance + cross-department integration. |

| 4 | Zscaler | ⭐⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐ | Very Low | Security control plane. AI increases cyber threats → more demand. Infra-layer business. |

| 5 | Vertiv | ⭐⭐⭐⭐ | ⭐ | ⭐⭐⭐ | Very Low | Physical AI infrastructure (data centers, cooling). Zero UI exposure. AI growth directly increases demand. |

| 6 | Atlassian | ⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ | Low | Engineering workflow backbone. Even with AI coding, teams need governance, tracking, compliance logging. Some seat risk, not structural collapse. |

| 7 | GitLab | ⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ | Low | DevOps lifecycle management. AI-generated code increases CI/CD complexity. Infrastructure-like positioning in software stack. |

| 8 | The Trade Desk | ⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐ | Low | AI-native ad bidding engine. Automation increases programmatic advertising scale. |

| 9 | Shift4 | ⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐ | Low | Payment rail. AI doesn’t replace transactions. Fraud detection improves with AI. |

| 10 | Remitly | ⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐ | Low | Cross-border transfer infrastructure. AI mainly enhances fraud control and compliance. |

| 11 | MercadoLibre | ⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐ | Low | Marketplace + fintech rails. AI improves logistics, targeting, and fraud detection. |

| 12 | Sea | ⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐ | Low | Ecommerce + gaming + fintech ecosystem. AI enhances operational efficiency. |

| 13 | Grab | ⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐ | Low–Medium | Superapp platform. AI optimizes dispatch, pricing, logistics. Not seat-based SaaS. |

| 14 | Netflix | ⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐ | Low–Medium | Content distribution platform. AI lowers production costs and improves recommendations. Not structurally attacked by AI. |

| 15 | Salesforce | ⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐ | Medium | Strong CRM SOR but tied to sales headcount. Seat compression possible if AI reduces sales teams. Execution pivot key. |

| 16 | Sezzle | ⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐ | Medium | BNPL financial product. AI largely irrelevant structurally. Risk more macro than AI-driven. |

| 17 | HubSpot | ⭐⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐ | Medium | Marketing automation for SMBs. AI commoditizes campaign creation. Higher seat compression risk. |

| 18 | Zeta Global | ⭐⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐ | Medium–High | Marketing tech platform vulnerable to AI-driven campaign automation tools. |

| 19 | Adobe | ⭐⭐⭐ | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | High | Creative UI-driven workflows. AI-native tools reduce need for manual design work. Engagement-heavy model exposed. |

| 20 | Duolingo | ⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐ | High | AI tutors can replicate structured language learning. Must deeply integrate AI to defend moat. |

| 21 | Udemy | ⭐⭐ | ⭐⭐⭐⭐⭐ | ⭐⭐ | Very High | Passive course marketplace. AI tutoring and personalized learning threaten core format. Weak SOR moat. |

| 22 | Upwork | ⭐ | ⭐⭐⭐⭐⭐ | ⭐⭐ | Extremely High | Marketplace for human labor. AI replaces entry-level coding, writing, design. Core demand structurally pressured. |

After much thought i will rule out all the high ai-disruption risk stocks as reinvestment candidate.

| Ticker | P/S | Gross Margin | Price / GP | AI Disruption Risk | Growth Conviction | Economic Moat (1–5) | Why This Deserves Conviction |

|---|---|---|---|---|---|---|---|

| MELI | 4.0x | 50.4% | 7.94x | Low | Very High | 5 | LATAM underpenetrated. Marketplace + fintech + logistics flywheel. AI improves operations, doesn’t replace demand. |

| GTLB | 4.2x | 88.0% | 4.77x | Low (AI Tailwind) | High | 4 | DevOps lifecycle control layer. AI increases code output → more CI/CD + security need. Elite 88% margin. |

| TTD | 4.1x | 78.8% | 5.20x | Very Low | Moderate–High | 4 | Independent DSP. AI-native optimization engine. Secular shift to CTV still ongoing. High margin compounder. |

| TEAM | 3.8x | 84.1% | 4.52x | Medium (Seat Compression Risk) | Moderate | 4 | Deep enterprise workflow embedment. AI may slow seat growth but governance demand remains. |

| SE | 2.7x | 44.9% | 6.01x | Low–Medium | Moderate | 3 | SEA ecommerce + fintech ecosystem. AI improves logistics; execution risk higher than MELI. |